Investor demand and housing price inflation.

Housing is unaffordable in Canada because the financial architecture conceived in the 1980s to increase home ownership and stimulate housing construction by leveraging private capital has, since the dot.com bubble collapsed in 2001 and investors turned their attention to housing, facilitated a housing price inflation so extreme that households are no longer able to pay more for it.

This inflation occurred in two waves. The first, from 2001 to 2008, was driven by institutional and individual investor demand for mortgage-backed securities to substitute on their balance sheets high-quality marketable debt for dot.com stocks which had mostly become worthless.

The second wave, from 2009 to 2022, was driven by near-zero Bank of Canada (BOC) overnight interest rates introduced initially to provide liquidity to Canada's financial system after the U.S. subprime mortgage bubble collapse in 2008 and continued until January, 2022 in order to prop up the massive housing bubble that ensued.

This second leg of Canada's housing price inflation occurred, as had the first, because variable rate mortgage (VRM) interest rates, which are set relative to bank's prime rates and therefore almost always move in lockstep with BOC overnight rate – in contrast to fixed-rate mortgage rates which in Canada are set relative to the 5-year bond yield – fell with BOC overnight rate and remained low until BOC overnight rate was finally raised in January, 2022.

Housing price inflation accelerated after 2009 because BOC overnight rate, which had bottomed at 2% in 2001 and 2004, plunged from 4.5% on November 9, 2007 to 0.25% on April 10, 2009, and essentially stayed there until January 8, 2022.

Inexpensive credit chases unearned income, and flooding commercial banks' mortgage window with 5-year VRM interest rates averaging 2.57% from 2009 to 2021 unleashed a torrent of speculation in Canada's housing markets.

To industrial capital, to "invest in housing" means to muster the resources necessary to house every Canadian adequately, securely, stably, and affordably. This is an investment in Canadians' future prosperity because it keeps the cost of living, and thus the cost of doing business – and prices – low (and competitive in international markets), as well as maximizing the vitality and morale of Canada's workforce.

To finance capital, to "invest in housing" means to repurpose housing from structures in which households dwell to financial assets whose function is either to be held and sold later at a higher price or used to extract economic rent from the productive economy in the present. Economic rent is unearned income and is not limited in any way by what it costs to produce a rent-extracting asset.

Financial investing includes loaning money – because a loan is an asset on the books of the lender – with the expectation it will be repaid with interest. Interest, capital gains, and rental income on properties beyond what it costs to own and maintain them are economic rents.

Variable rate mortgages and mortgage-backed securities.

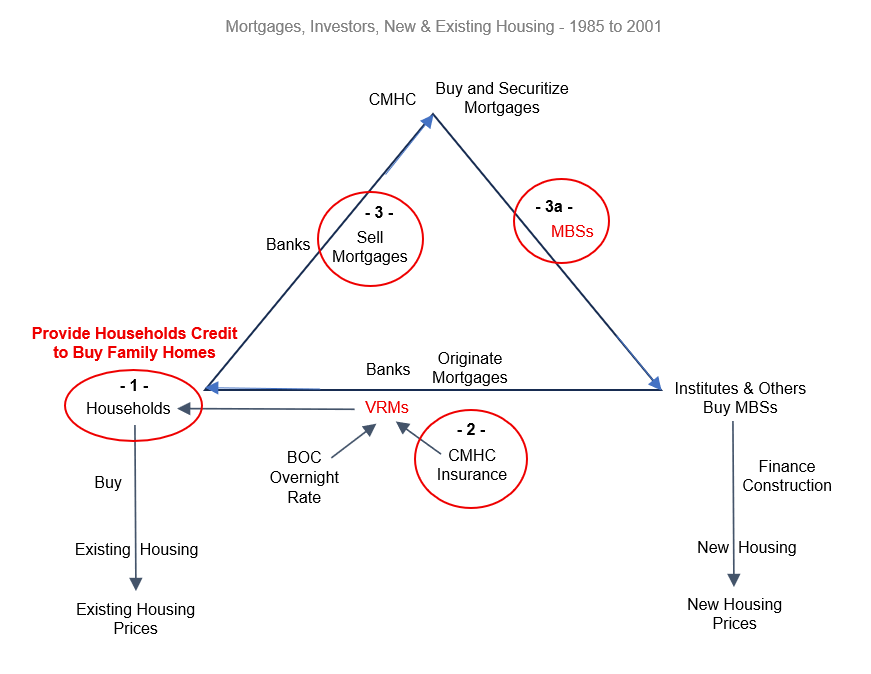

Figure 1 illustrates the financial architecture implemented in Canada beginning in the 1950s and culminating in the 1980s to increase home ownership and stimulate housing construction.

Public statements (page 4) by leaders involved in designing this system make clear that their motive truly was to improve Canadians' access to adequate, secure, stable, affordable, housing.

They succeeded in this in no small measure due to the simplicity of this design, the basic architecture of which is still in place today; and they generalized this access by building more than 600,000 units of publicly financed, not-for-profit housing from 1968 to 1993.

Impacts of the policies introduced from 1954 to 1985.

The CMHC mortgage loan insurance program was introduced in 1954 when the National Housing Act of 1938 – enacted during the depression to provide financial support for home construction, repair, and modernization – was expanded with the objective of making home ownership more accessible to Canadians by encouraging chartered banks to offer mortgage loans and insuring those loans against borrower default. This allowed homebuyers to purchase a home with a lower down payment than had previously been required.

The introduction of VRMs in the 1970s, and their subsequent insurance by CMHC in 1982, is central to the story of the housing price inflation that occurred in Canada from 2001 to 2022 because VRMs, which enable lenders to transfer interest rate risk to borrowers, are offered at lower interest rates than fixed-rate mortgages.

To offer this discount, VRM interest rates – in contrast to those of fixed rate mortgages, which are set relative to long-term bond yields (usually the 5-year bond yield in Canada) – are set relative to lenders' prime rates, which themselves are typically set 1.5 to 2.5 percentage points above and closely follow BOC overnight rate.

Extending NHA insurance coverage to include VRMs in 1982 helped banks and trust companies make VRMs more widely available.

In 1985, CMHC introduced the NHA Mortgage-Backed Securities (MBS) program to help develop Canada's securitization market by unconditionally guaranteeing payments on pools of insured mortgages (fixed rate only), making them attractive to a wide range of investors.

The NHA MBS program offloaded default risk from mortgage issuers by enabling them to sell mortgages they originate to CMHC, which bundles them into MBSs.

All of these policy changes together, by leveraging demand by finance capital for low-risk investment instruments and enabling banks to offload particular risks associated with originating mortgages, created conditions that enabled households seeking a family home to find financing for that purpose, as well as incentivizing investment in new housing construction.

With few exceptions, homeowners during the period 1985 to 2001 who "traded up" to another house to accommodate a growing family or for other reasons sold the one they currently owned. Similarly, condo pre-buyers during this period took advantage of the discount developers offer to attract financing to move into more practical or agreeable surroundings.

When the dot.com bubble collapsed.

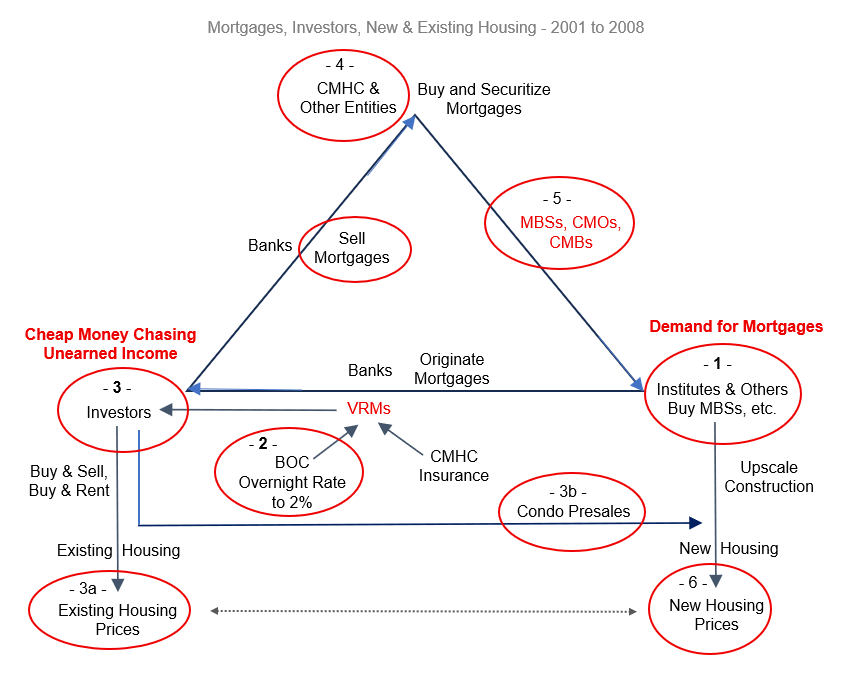

In Canada after the dot.com bubble collapsed in 2000-2001, investor demand for MBSs increased dramatically not only because investors have always considered MBSs low-risk instruments – because homeowners prioritize paying their mortgages and renters paying their rents – but also because actual households paying off mortgages on actual homes seemed more solidly grounded than dot.com fantasies that had vanished without a trace.

Figure 2 illustrates that – in contrast to the period 1985 to 2001, when demand by households for access to mortgages to finance homeownership drove, in order: insuring VRMs, decreasing BOC overnight rate, and establishing a secondary mortgage market – mortgage securitization in Canada after the collapse of the dot.com bubble was driven instead by demand among large financial institutions for mortgages, MBSs, and derivatives as sources of government-guaranteed income. BOC, responding to the slowdown in the U.S. economy, coincidentally slashed its overnight rate, dragging VRM interest rates lower,

Impacts of the policies introduced from 2001 to 2008.

To accommodate demand among institutional investors for government-guaranteed income-generating assets, CMHC began pooling MBSs into Canada Mortgage Bonds (CMBs) in 2001 (sequential page 12).

Also, under a pilot program in 2003/2004 and with full implementation effective December 1, 2004, CMHC expanded its MBS program, which had been restricted to include only fixed-rate mortgages when it was introduced in 1985, to include VRMs. By 2004, VRMs were fully incorporated into MBSs and, by extension, CMBs.

BOC, in response to the slowdown in the U.S. economy following the dot.com bubble collapse, reduced its overnight rate, which was 5.75% on January 1, 2001, to as low as 2%, which it touched on January 14, 2002, for the first time since 1955.

This in turn drove VRM interest rates low enough to attract interest to housing as a sector in which easy money could be made, and banks' mortgage windows began increasingly to serve a variety of investors in addition to households seeking financing to purchase a family home.

These included speculators taking advantage of inexpensive credit to buy and flip houses, condos, and townhouses; and new and experienced investors purchasing and putting into service as long- and short-term rentals (LTRs and STRs) housing units that had been proposed, approved, and built with the understanding they would be owned by the households occupying them.

In addition, after 2001, inexpensive mortgages, coupled with rapidly increasing housing prices, made it more financially attractive for households buying a new home to hold onto and rent out their current one to accumulate equity paid for by their tenants than to sell it.

Condo buyers, similarly after 2001, increasingly leveraged presale discounts to acquire income-producing properties or to resell at a profit, as opposed to buying condos in which to reside. Condo developers, to accommodate this market, began incorporating units into their buildings – "postage stamps" – specifically designed to be rented.

This trend led ultimately to developers proposing so-called "micro-lofts" to City Councils as a "new trend" in urban living. It does not take much insight to realize these are actually unregulated hotel rooms marketed deceptively as full-time residences.

Because a lower interest rate finances a larger principle and a speculator's mortgage is paid not by themselves but by a tenant, short-term guests, or a property's next buyer, speculators outbidding households who would pay their own mortgages drove a housing price inflation during this period that resulted in housing prices increasing 67% from 2001 to 2008.

"End-users" and renters, at the mercy of "market rates" and none of whom would willingly forgo housing and live on the street, had no alternative but to pay the price for this housing price inflation.

The almost inflationary-neutral system conceived in the 1980s to increase households' access to a family home was predicated on the assumption that it is households seeking dwellings that buy housing. Because no provision was made to prevent middlemen from buying up, then flipping, renting out, or repurposing as unregulated hotels new and existing housing that came online, this arrangement became the engine of an out-of-control inflation in housing prices and monthly rents.

Banks were more than happy to go along with this because the more mortgages one writes, and the bigger those mortgages are, the fatter one's bottom line.

When the U.S. subprime mortgage bubble collapsed.

In the U.S. during the period 2001-2008, investor demand for MBSs and their newly invented derivatives, which included collateralized debt obligations (CDOs) and a variety of mortgage-backed bonds, was so great that mortgage originators in the U.S. sent armies of salesmen door-to-door, particularly in minority neighbourhoods, to sell adjustable rate mortgages (ARMs) to unsuspecting homeowners who would not be able to make their payments when the teaser period on their loans was over. (See Aaron Glanz and Bill Black [Part 3] for more.)

The financial crisis that followed the U.S. subprime mortgage bubble collapse thrust Canada's largest trading partner into a "Great Recession." In response to crashing commodity prices, weakening exports, and diminishing U.S. investment in Canada, BOC slashed its overnight rate, which reached 0.25% in April 2009 and essentially remained there until January, 2022.

Near-zero BOC overnight rates preserved the viability of VRM mortgages sold prior to 2008, the banks that issued them, and the institutions holding the MBSs and CMBs containing them by enabling those VRMs to be reset at a lower rate.

Figure 3 illustrates that ultra-low BOC overnight rates helped to inflate housing prices further by plunging the average interest rate on a VRM, in 2009 for example, to as low as 1.95%.

Mortgage rates this low emboldened flippers, short- and long-term lessors, and land- and housing-accumulators to "invest" with increasing confidence in existing housing and condo presales.

Since a lower interest rate enables a determined investor to borrow a larger principal for the same number of dollars, housing prices rose precipitously and continued rising for another 13 years, until end-users' and renters' paychecks were finally unable to keep up.

Skyrocketing housing prices and rents propelled by accelerating investor demand and extremely low VRM interest rates encouraged debt and equity investors to increase their involvement in financing new housing construction, all of which was as upscale as possible, not only because high-priced housing yields bigger returns, but – more to the point – for-profit developers cannot build affordable housing.

Housing price inflation after 2008.

From 2008 to 2022, government, CMHC, and BOC policies worked together, sometimes inadvertently, sometimes not, to prop up and continue Canada's worsening housing price inflation.

The narrative pounded into Canadians' minds by mass media, politicians, and sell-side FIRE (Finance, Insurance, and Real Estate) sector marketers is not that the root cause of Canada's housing price inflation is the financial architecture put in place in the 1980s to minimize the price of housing having been coopted by a vast financial apparatus seeking to maximize it but that "demand" by households for structures in which to dwell, exacerbated by the presence of "immigrants" also needing to be housed, has outstripped the "supply" of housing.

Increasing "supply," particularly of "market rate" housing, is relentlessly insisted to be the way to make Canadian housing affordable again, and the nation has embarked on a mission to "increase supply" rather than to correct the root cause of Canada's housing price inflation, namely the financialization of housing in Canada.

The purely imaginary concept of "filtering" – that is, the claim that as households move up from affordable housing into newer, more expensive units, others would occupy the affordable units they left vacant – was cooked up to justify building ever more expensive housing.

What actually occurred is that 550,00 units of affordable rental housing were bought by real estate holding corporations and converted to "market rate" rentals between 2011 and 2021.

Affordable housing units were demolished during this period as well to make way for new, upscale housing, a number no national data source tracks. Another number that is real but difficult to quantify is units of affordable housing lost when their holders, emboldened by increasing rents nearby, demand more for their properties because "rents are going up."

Government implemented policies during this period to make housing more "affordable" that did nothing to reduce its price. These include first-time buyer subsidies and supports that enable renters to pay "market rate," both of which amount to pass-through subsidies; that is, vehicles that transfer public dollars into the hands of holders on behalf of nominal beneficiaries. These dollars prop up exorbitant rents on the one hand and, for those landing in the hands of house and condo sellers, exorbitant house and condo prices on the other.

There is only one way to build affordable housing, and that is to build affordable housing.

Even though finance capital is turning its attention to other sectors because little, if any, upside remains in housing, building affordable housing still faces formidable political opposition from homeowners who have paid through the nose for their properties or are enjoying multimillion-dollar appreciation as well as, obviously, real estate holding corporations, banks, and other financial institutions whose business model, and in some cases their very existence, depends on housing prices not retracing further.

The dilemma finally comes down to definancializing housing, eliminating middlemen, and deflating Canada's housing bubble without crashing the Canadian economy.